|

|

|

|

|

|

1.

|

Study the information above.

What do you expect to learn from this module? Enter your answer on the right. Also, review the

vocabulary words and look for them as you work through this lesson. You will be tested on them

later.

|

|

|

Economists say that a market will tend

toward equilibrium, which means that

the

price and quantity will gradually move

toward their equilibrium levels. Why does

this happen?

Remember that excess

demand will lead firms to raise prices.

Higher prices induce the quantity

supplied

to rise and the quantity demanded to fall

until the two values are equal.

On

the other hand, excess supply will

force firms to cut prices. Falling prices will

cause

quantity demanded to rise and

quantity supplied to fall until, once again,

they are equal.

Through these relationships,

the market price and quantity sold

of a good will move toward

their equilibrium

values.

|

Remember from Chapters 4 and 5 that

all of the

changes in demand and supply

described above are changes along a

demand or supply curve.

Assuming that a

market starts at equilibrium, there are two

factors that can push it into

disequilibrium:

a shift in the entire demand curve

and a shift in the entire supply

curve

| | |

|

|

|

2.

|

What do companies do when there is excess demand for a

product?

a. | lower

prices | c. | nothing | b. | raise prices | d. | change the product |

|

|

|

3.

|

What happens to the supply of a

product when prices rise?

a. | The company will produce more of the

product, supply will increase | c. | The company will do nothing | b. | The company will produce less of the product, supply will

decrease | d. | The company will reduce

prices |

|

|

|

4.

|

What happens when the quantity

of a product increases along with an increase in prices?

a. | demand for the product will

increase | c. | there will be no

change in supply or demand | b. | demand for the product will decrease | d. | prices will rise even more |

|

|

|

5.

|

What happens to the market when

the supply for a product equals the demand for the product?

a. | the market is in

disequilibrium | c. | the market is

falling | b. | the market is in equilibrium | d. | the market is rising |

|

|

|

| Factors that reduce supply shift the supply curve to the

left, while factors that increase supply move the supply curve to the

right. | Changes in

Price

In Chapter 5, you

read about the different

factors that shift a supply curve to the left

or to the right. These

factors include

advances in technology, new government

taxes and subsidies, and changes in

the

prices of the raw materials and labor used

to produce the

good.

| Since market

equilibrium occurs at the

intersection of a demand curve and a

supply curve, a shift of the

entire supply

curve will change the equilibrium price and

quantity. A shift in the supply curve

to the

left or the right creates a new equilibrium.

Since markets tend toward equilibrium,

a

change in supply will set market forces into

motion that lead the market to this

new

equilibrium price and quantity sold. | | |

|

|

|

6.

|

Where does market equilibrium

occur in a chart?

a. | The lowest point on the demand and

supply curve | c. | The highest point

on the supply curve | b. | The highest point on the demand curve | d. | The point at which the supply curve and the demand curve

cross |

|

|

|

7.

|

What can cause a change in the

price of a product? (select all that apply)

|

|

|

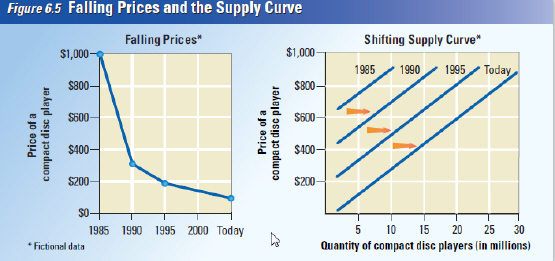

As CD players become cheaper to produce, the supply increases at all

but the lowest prices. | Understanding a Shift in Supply

When compact disc players were first introduced in the

early 1980s, a basic, single-disc machine cost around $1,000. The early compact disc players were

much more expensive and less sophisticated than the compact disc players people use today. Gradually,

as firms developed better technology for producing compact disc players, their prices fell. In 1990,

a consumer could purchase a fancy single-disc player for $300; just five years later, in 1995, a

similar player could be purchased for about $200. Today, consumers can buy a compact disc player for

less than $100.

Not only have the prices of compact disc players fallen, but the machines on

sale today have many more features and options than the original $1,000 machine. .

| Technology has

lowered the cost of manufacturing compact disc players and has also reduced the costs of some of the

inputs, like computer chips. These advances in production have allowed manufacturers to produce

compact disc players at lower costs. Producers have passed on these lower costs to consumers in

the form of lower market prices

We can use the tools developed in Chapter 5 to graph the

effect of these changes on the CD market? ’s supply curve. Figure 6.5 shows how the supply

curve shifted outward, or to the right, as manufacturers offered more and more CD players at lower

prices. In the early 1980s, no compact disc players were offered for $300. They were simply too

expensive to develop and manufacture. Today, manufacturers can offer millions of CD players at this

price. | | |

|

|

|

8.

|

What factor is most important

in reducing the cost and quality of CD players through the years.

a. | More people are listening to music

than before | c. | Technology has

reduced the cost and improved the quality of CD Players | b. | Hip Hop and Rap are better music than classical

music | d. | More people can afford CD

Players |

|

|

|

9.

|

Technology has reduced the cost

of CD players by lowering the cost of manufacturing. What other factor has technology helped to

reduce cost?

a. | component

parts | c. | marketing in multiple outlets such

as Costco | b. | advertising the product | d. | the popularity of country/western

music |

|

|

|

10.

|

Normally demand will influence

the supply of a product until an equilibrium point is reached between supply and demand. What happens

to the supply curve if an outside force, such as technology, influences both supply and demand

causing them both to increase?

a. | the demand and supply curve will

shift to the left | c. | supply will

decrease | b. | the demand and supply curve will shift to the

right | d. | demand will decrease while supply

increases |

|

|

|

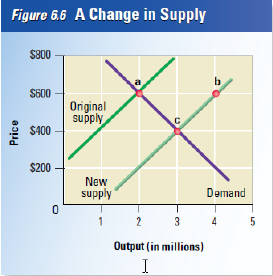

Finding a

New Equilibrium

Picture

the point in time when compact disc players were evolving from an expensive luxury good to a

mid-priced good. A new generation of computer chips has just reduced the cost of production. These

lower costs have shifted the supply curve to the right where at each price, producers are willing to

supply a larger quantity.

This shift, shown in Figure 6.6 using fictional quantities, has

thrown the market into disequilibrium. At the old equilibrium price, suppliers are now willing to

offer 4,000,000 compact disc players, up from 2,000,000.

In Figure 6.6, the increase in

quantity supplied at the old equilibrium price is shown as the change from point a to point b.

However, the quantity demanded at this price has not changed, and consumers will only buy 2,000,000

compact disc players. At this market price, unsold compact disc players will begin to pile up in the

warehouse. When quantity supplied exceeds quantity demanded at a given price, economists call this a

surplus. The surplus compact disc players are excess supply, so something will have to change

to bring the market to equilibrium.

As you read in Section 1, suppliers will respond to excess

supply by reducing prices. As the price falls from $600 to $400, more consumers decide to buy compact

disc players, and the quantity demanded rises. The combined movement

| of falling

prices and increasing quantity demanded can be seen in Figure 6.6 as a change from point a to

point c. Notice that this change is a movement along the demand curve, not a shift of the entire

demand curve.

Eventually, the price falls to a point where quantity supplied and quantity

demanded are equal, and excess supply is no longer a problem. This new equilibrium point, shown at

point c in Figure 6.6, marks a lower equilibrium price and a higher equilibrium quantity sold than

before the supply curve shifted. This is how equilibrium changes when supply increases, and the

entire supply curve shifts to the right.

When supply increases, prices fall, and quantity

demanded increases to reach a new equilibrium. When supply increases, prices fall, and quantity

demanded increases to reach a new equilibrium. | | |

|

|

|

11.

|

How do producers react when

production costs have decreased because of technology?

a. | producers decrease the supply

| c. | producers do nothing because of

price instability | b. | producers increase the supply | d. | producers try to avoid the cost of

technology |

|

|

|

12.

|

What do economists call it when

supply exceeds demand?

a. | equilibrium | c. | surplus | b. | shortage | d. | cost |

|

|

|

13.

|

When supply changes from point

a to point b we have a situation called

a. | equilibrium | c. | surplus | b. | excess demand | d. | shortage |

|

|

|

14.

|

What has to happen to the chart

above to reach market equilibrium?

a. | new technology will have to be

introduced to increase supply | c. | the price moves to a point where quantity supplied and quantity demanded are

equal | b. | new technology will have to be avoided | d. | the price falls to a point where quantity supplied and quantity demanded are

equal |

|

|

|

15.

|

Market equilibrium is

illustrated in the chart above by points

a. | a and b | c. | b and c | b. | a and c | d. | equilibrium is not illustrated on this

chart |

|

|

|

16.

|

What happened when the supply

curve shifted from point a to point c?

a. | lower price and greater

supply | c. | increased supply and

price | b. | lower supply but greater price | d. | lower supply and price |

|

|

|

A Fall in

Supply

Just as new

technology or lower costs can shift the supply curve to the right, so other factors that reduce

supply can shift the supply curve to the left. Consider the market for cars. If the price of steel

rises, automobile manufacturers will produce fewer cars at all price levels, and the supply curve

will shift to the left. If auto workers strike for higher wages, and the company must pay more for

labor to build the same number of cars, supply will decrease. If the government imposes a new tax on

car manufacturers, supply will decrease. In all of these cases, the supply curve will move to the

left, because the quantity supplied is lower at all price levels.

| When the supply

curve shifts to the left, the equilibrium price and quantity sold will change as well. This process

is the exact opposite of the change that results from an increase in supply. As the supply curve

shifts to the left, suppliers raise their prices and the quantity demanded falls. The new equilibrium

point will be at a spot along the demand curve above and to the left of the original equilibrium

point. The market price is higher than before, and the quantity sold is

lower | | |

|

|

|

17.

|

What will happen to the supply

curve if production costs rise dramatically?

a. | Will shift to the

right | c. | Will remain

stationary | b. | Will shift to the left | d. | Will move to the right and left |

|

|

|

18.

|

What happens as the supply

curve shifts to the left?

a. | suppliers raise their prices and the

quantity demanded also rises | c. | suppliers raise their prices and the quantity demanded

falls | b. | suppliers lower their prices but there is no change in the quantity

demanded | d. | suppliers lower their prices and the

quantity demanded falls |

|

|

|

19.

|

If the market price is higher

than before, what will happen to the quantity sold

a. | will also be

higher | c. | will remain the

same | b. | will be lower | d. | market prices can never be

higher |

|

|

|

20.

|

What are some of the production

costs that can cause a shift in the supply curve? (click all that apply)

|

|

|

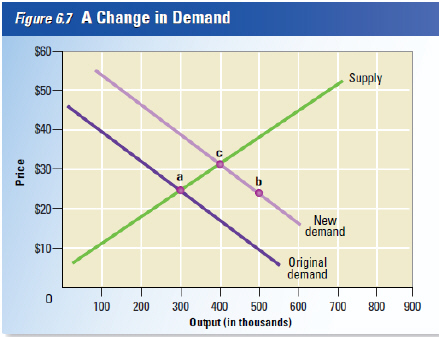

Shifts in

Demand

Almost every

year, around November, a

new doll or toy emerges as a nationwide

fad. People across the country

race to

stores at opening time and stand in long

lines to buy that year’s version of

Tickle

Me Elmo or Pokmon.

As you read in Chapter 4, these fads

reflect the impact of

consumer tastes and

advertising on consumer behavior. Fads

like these, in which demand rises

quickly,

are real-life examples of a rapid, rightward

shift in a market demand curve.

Figure

6.7 shows how a rapid, unexpected

increase in market demand will affect the

equilibrium in a

market for a hypothetical,

trendy toy.

The Problem of Excess

Demand

In Figure 6.7, the fad causes a sudden

increase in market demand, and

the

demand curve shifts to the right. This shift

leads to excess demand at the

original

price of $24 (point b). Before the fad

began, quantity demanded and

quantity

supplied were equal at 300,000 dolls,

shown at point a. On the graph,

excess

|

In the stores that carry the dolls, excess

demand appears as bare

shelves and long

lines. Excess demand also appears in the

demand appears as a gap between

the

quantity supplied of 300,000 dolls and the

new quantity demanded of 500,000 at

$24,

shown at point b. This is an increase

of 200,000 in the quantity demanded.

Economists would

also describe this as a

shortage

of 200,000 dolls.

In the stores that carry the dolls excess demand appears in the form of

search costs—the financial and opportunity costs consumers pay in searching for a good

or service. Driving to different stores and calling different towns to find an available doll are

both examples of search costs.

In the meantime, the available dolls must

be rationed, or

distributed, in some other

manner. In this case, long lines, limits on

the quantities each

customer may buy, and “first come, first serve” policies are used to

distribute the

dolls among customers.

| | |

|

|

|

21.

|

As illustrated in the chart

above an unexpected demand for a new doll will cause the demand curve to

a. | shift to the

right | c. | remain

static | b. | shift to the left | d. | be in equilibrium |

|

|

|

22.

|

In the example above, you

really want the doll in question and have to spend a great deal of time searching for it in multiple

stores. This is an example of

a. | excess supply

| c. | technological

innovation | b. | a production cost | d. | an opportunity cost |

|

|

|

23.

|

Excess demand which causes the

demand curve to shift to the right will

a. | lower

price | c. | cause price to remain the

same | b. | increase price |

|

|

|

24.

|

As the equilibrium in the chart

above shifts from a to c, output changes from

a. | $25 to

$30 | c. | 300 to

400 | b. | $5 to $55 | d. | 300 to 500 |

|

|

|

| Return to

Equilibrium

As time

passes, firms will react to the signs of excess demand and raise their prices. In fact, customers may

actually push prices up on their own if there is “bidding? ” in the market, as there is

for real estate, antiques, fine art, and hard-to find items.

If a parent cannot find the doll

he wants at the store, he might offer the store keeper an extra $5 to guarantee him a doll from the

next shipment. Through these methods, the market price will rise until the quantity supplied equals

the quantity demanded at 300,000 dolls. All of these dolls are sold at the new equilibrium price of

$30, shown at point c in Figure 6.7.

When demand increases, both the equilibrium price and the

equilibrium quantity also increase. The demand curve has shifted, and the equilibrium point has

moved, setting in motion market forces that push the price and quantity toward their new equilibrium

values. | A Fall in Demand

When a fad passes its peak, demand can fall as quickly as it rose. Excess demand turns

into excess supply for the once popular toy as parents look for a new, more trendy gift for their

children. Overflowing store shelves and silent cash registers, the symptoms of excess supply, replace

long lines and bidding wars.

When demand falls, the demand curve shifts to the left. Suppliers

respond by cutting prices on their inventory. Price and quantity sold slide down along the supply

curve to a new equilibrium point at point a in Figure 6.7. The end of the fad restores the original

price and quantity supplied.

Now that you understand economics it is time for

your generation to make some changes

| | |

|

|

|

25.

|

As the demand curve has shifted

and the equilibrium point moves, market forces will push the price and quantity

a. | toward their new equilibrium

values | c. | to remain

static | b. | toward their new disequilibrium

value |

|

|

|

26.

|

If people suddenly loose

interest in the new doll, demand can fall quickly

a. | and supply and demand will become

frozen along the demand supply curve | c. | and excess supply can turn into excess

demand | b. | supply and demand will reach equilibrium | d. | and excess demand can turn into excess

supply |

|

|

|

27.

|

This section illustrates the

fact that suppliers

a. | react to market forces causing an

equilibrium in supply and demand | c. | react slowly to market forces that effect supply and

demand | b. | react to market forces causing a disequilibrium in supply and

demand | d. | usually ignore market forces that effect supply and

demand |

|