|

|

|

|

|

|

1.

|

Examine the information above.

What do you expect to learn in this lesson? Enter your answer in the space on the right.

Review

the vocabulary words for this section. Look for them as we work through this section. You will be

tested on them later

|

|

|

The law of supply predicts that higher prices lead to more

production.

The Law of Supply

Supply is the amount of goods available.

How do

producers decide how much to

supply? According to the law of supply, the

higher the

price, the larger the quantity

produced. Economists use the term quantity

supplied to

describe how much of a good is

offered for sale at a specific price.

The law of supply

develops from the

choices of both current and new

producers of a good. As the price of

a

good rises, existing firms will produce

more in order to earn additional

revenue.

|

At the same time, new firms will have an

incentive to enter the market

to earn a

profit for themselves. If the price of a good

falls, some firms will produce less,

and

others might drop out of the market. These two movements—individual firms

changing

their level of production and

firms entering or exiting the market—

combine to create the

law of supply. | | |

|

|

|

2.

|

What does the law of supply

predict?

a. | higher prices will lead to less

production | c. | more supply will

lead to higher prices | b. | higher prices will lead to more production | d. | supply has no effect on production or

demand |

|

|

|

3.

|

How is the law of supply

different from the law of demand?

a. | An increase in price equals an

increase in supply and a decrease in demand | c. | A decrease in price equals an increase in supply and a decrease in

demand | b. | An increase price equals a decrease in supply and

demand | d. | There is no difference in the law of supply and

demand |

|

|

|

4.

|

What term do economists use to

describe how much of a good is offered for sale at a specific price?

a. | price

ratio | c. | quantity

demanded | b. | price demanded | d. | quantity supplied |

|

|

|

5.

|

Why do firms produce more when

prices rise?

a. | They want to share their

wealth | c. | They want to earn more

money | b. | They want to make prices fall | d. | They do not want to overproduce |

|

|

|

Higher

Production

If a firm

is already earning a profit by

selling a good, then an increase in the

price—ceteris

paribus—will increase the firm’s profits. The promise of higher revenues for each

sale also encourages the firm to produce more. Consider the pizzeria you read about in Chapter 4. The

pizzeria is probably making a reasonable profit by selling a certain number of slices a day at the

market price. If the pizzeria weren’t making a profit, the owner would soon try to raise the

price or switch from pizzas to something more profitable.

If the price of pizza rises, but the

firm’s cost of making pizza stays the same, then the pizzeria will earn a higher profit on each

slice of pizza. A sensible entrepreneur would try to produce and sell more pizza to take advantage of

the higher prices.

| Similarly, if the price of pizza goes down, the pizzeria will earn less profit

per slice or even lose money. The owner will choose to sell less pizza and produce something

else, such as calzones or sandwiches, that will yield more profit.

In both cases, the search

for profit drives the supplier’s decision. When the price goes up, the supplier recognizes the

chance to make more money and works harder to produce more pizza. When the price falls, the same

entrepreneur is discouraged from producing as much as before.

| | |

|

|

|

6.

|

If a company were selling a

product and suddenly the price of the product increased, what action would the company likely

take?

a. | They would decrease supply to

increase demand | c. | They would produce

less of the product (decrease supply) | b. | They would produce more to lower the price | d. | They would produce more of the product (increase

supply) |

|

|

|

7.

|

What motivation drives the

behavior of business persons?

a. | taking less

risk | c. | making more

money | b. | taking more risk | d. | increasing price |

|

|

|

Market

Entry

Profits appeal

both to producers already in

the market and people who may decide to

join the market. As you

have seen, when

the price of pizza rises, a pizzeria stands out

as a good opportunity to make

money. If

you were considering opening a restaurant

of your own, a pizzeria would look like

a

safe bet. In this way, rising prices draw new

firms into a market and add to the

quantity

supplied of the good.

Consider the market for music. In the

late 1970s, disco

music became popular

among young people. The music industry

quickly recognized the popularity

of disco,

and more and more groups began releasing

disco recordings. Even some groups

that

once performed soul music and rhythm

and blues chose to record disco albums.

New

entrants crowded the market to take

advantage of the potential for profit. Disco,

however,

proved to be a short-lived fad. By

the early 1980s, disco music was gone from

the radio, and

stores couldn’t sell the

albums on their shelves.

This pattern of sharp increases

and

decreases in supply occurs again and again

in the music industry. In the early

1990s,

“grunge” music emerged from Seattle to

become widely popular among high

school

and college students across the country.

How did the market react? Record labels

soon

hired many grunge groups. Music

stores devoted more and more space to this

style of music.

Within a few years,

however, grunge lost its appeal, and many

groups disbanded or moved on to

new

styles. Other styles of music, such as salsa,

achieved new

popularity.

|

In each of the examples above, many

musicians joined the market for

a particular

style of music to profit from a trend.

Their actions reflected the law of

supply,

which says that the output or quantity

supplied of a good increases as the price

of

the good increases.

Grunge

Fashion | | |

|

|

|

8.

|

You are a young man who has

some money and is thinking about starting a business in sporting goods. You notice that there has

been a sharp decline in the prices of bogy boards and skate boards, while the price of surf

boards has remained about the same. You also notice that there has been a rise in the price of snow

boards over the past year. Since your goal is to make lots of profits, which item are your likely to

feature in your new sporting goods store?

a. | bogy

boards | c. | snow

boards | b. | surf boards | d. | skate boards |

|

|

|

9.

|

In the discussion above, what

do we learn about music?

a. | Young people can’t make up

their minds about the type of music they like. | c. | Musicians tend to play the most popular form of music because like any other

business person they want to make money | b. | It is better to become a classical musician because classical music is always

with us. | d. | Hip Hop, Disco, Grunge, Rap, Rhythm

and Blues, and Heavy Metal are not good forms of music because their popularity does not

last |

|

|

|

This supply schedule lists how many slices of pizza one pizzeria will

offer at different prices.

The

Supply Schedule

Similar

to a demand schedule, a supply

schedule shows the relationship between

price and

quantity supplied for a specific

good. The pizzeria discussed earlier might

have a supply

schedule that looks like the

one in Figure 5.2. This table compares two

variables, or

factors that can change. These

variables are the price of a slice and the

number of slices

supplied by a pizzeria. We

could collect this information by asking the

pizzeria owner how many

slices she is

willing and able to make at different prices,

or we could look at records to see

how the

quantity supplied has varied as the price

has changed. We will almost certainly

find

that at higher prices, the pizzeria owner is

willing to make more pizza. At a

lower

price she prefers to make less pizza and to

devote her limited resources to other,

more

profitable, items.

|

Like a demand schedule, a supply

schedule lists

supply for a very specific set

of conditions. The schedule shows how the

price of pizza, and

only the price of pizza,

affects the pizzeria’s output. All of the other

factors that

could change the restaurant’s

output decisions, such as the costs of tomato sauce, labor,

and rent, are assumed

to remain constant.

| | |

|

|

|

10.

|

What does this chart tell you

about the pizzeria owner’s decisions?

a. | He will produce more slices as the

price increases. | c. | He will make the

same amount of money no matter what the price is | b. | He will produce fewer slices as the price

increases | d. | Pizza restaurant owners are not good

business people |

|

|

|

11.

|

Many factors can influence the

supply of pizza. The supply schedule shows only one factor. What is it?

a. | cost of tomato

sauce | c. | rent | b. | labor | d. | price of pizza

|

|

|

|

A Change in the Quantity

Supplied

Economists use

the word supply to refer to

the relationship between price and quantity

supplied, as

shown in the supply schedule.

The pizzeria’s supply of pizza includes all

possible

combinations of price and output.

According to this supply schedule, the

pizzeria’s

supply is 100 slices at $ .50 a

slice, 150 slices at $1.00 a slice, 200 slices

at $1.50 a

slice, and so on. The number of

slices that the pizzeria offers at a specific

price is called

the quantity supplied at that

price. At $2.50 per slice, the pizzeria’s

quantity supplied

is 300 slices per day.

| A rise or fall in the price of pizza will

cause the quantity supplied to

change, but

not the supply schedule. In other words, a

change in a good’s price moves the

seller

from one row to another in the same

supply schedule, but does not change the

supply

schedule itself. When a factor other

than the price of pizza affects output, we

have to build a

whole new supply schedule

for the new market conditions. | | |

|

|

|

12.

|

What do we call the number of

slices of pizza at a specific price?

a. | supply

demanded | c. | quantity

demanded | b. | quantity supplied | d. | ratio of price to demand |

|

|

|

13.

|

What does the economist have to

do when a factor other than the price of pizza affects output?

a. | go back and rely on

demand | c. | nothing can affect supply other than

price | b. | build a new supply schedule for the new

condition | d. | divide the price by the supply times

100 and create a new schedule |

|

|

|

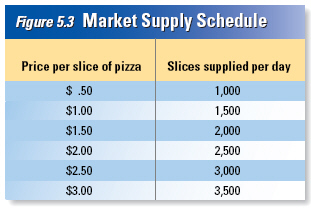

A market supply schedule represents all suppliers

in a market.

Market Supply Schedule

All of the supply schedules of individual

firms in a

market can be added up to create

a market supply schedule. A market supply

schedule

shows the relationship between

prices and the total quantity supplied by all firms in a particular

market. The information

in a market supply schedule becomes

important when we want to determine

the

total supply of pizza at a certain price in a

large area, like a city.

The market

supply schedule for pizza

resembles the supply schedule at a single

pizzeria, but the

quantities are much larger.

Figure 5.3 shows the supply of pizza for a

hypothetical

city.

This market supply schedule lists the

same prices as those in the supply

schedule

for the single pizzeria, since all restaurants

will charge prices within the same

range.

The quantities supplied are much larger

because there are many pizzerias in

the

community. Like the individual supply

schedule, this market supply schedule

reflects the

law of supply. Pizzerias supply

more pizza at higher prices.

| | | |

|

|

|

14.

|

In figure 5.2 you saw the

supply schedule for an individual pizzeria, such as Little Caesar’s. What if you wanted to

create a supply schedule for all of the Little Caesar’s in San Diego? What would we call that

new supply schedule for an entire city?

a. | market supply

schedule | c. | supply vs price

schedule | b. | supply schedule | d. | demand schedule |

|

|

|

15.

|

In figure 5.2 you saw the

supply schedule for an individual pizzeria, such as Little Caesar’s. What if you wanted to

create a supply schedule for all of the Little Caesar’s in San Diego? How would this new supply

schedule for a city differ from an individual Little Caesar’s store?

a. | The quantities supplied would be

much larger | c. | The prices would

be much larger | b. | The quantities demanded would be much larger | d. | The prices would be much smaller |

|

|

|

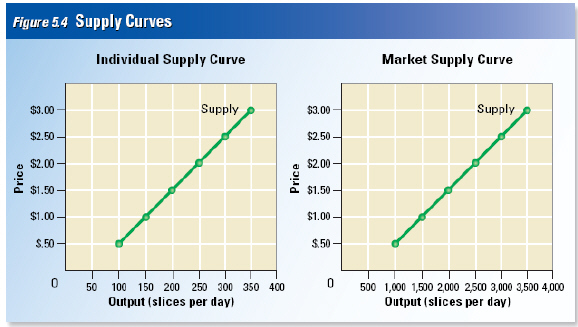

Supply

curves always rise from left to right, as predicted by the law of supply. As price increases, so does

the quantity supplied. Supply

curves always rise from left to right, as predicted by the law of supply. As price increases, so does

the quantity supplied.

The

Supply Graph

When

the data points in the supply

schedule are graphed, they create a supply

curve. A supply

curve is very similar to a

demand curve, except that the horizontal

axis now measures the

quantity of the good

supplied, not the quantity demanded.

Figure 5.4 shows a supply curve for

one

pizzeria and a market supply curve for all the pizzerias in the city. The data used to

draw the two curves are from the supply schedules in Figures 5.2 and 5.3. The prices

| shown

along the vertical axes are the same

in both graphs. However, the quantities of

pizza supplied

at each price are much larger

in the market supply curve.

The key feature of the supply

curve is

that it always rises from left to right. As

your finger traces the curve from left

to

right, it moves toward higher and higher

output levels (on the horizontal axis)

and

higher and higher prices (on the vertical

axis). This illustrates the law of

supply,

which says that a higher price leads to

higher output. | | |

|

|

|

16.

|

Why do supply curves always

rise from left to right.

a. | because price and quantity supplied

rise together | c. | because supply and

demand fall together | b. | because price rises while supplies fall | d. | because supplies rise while price

falls |

|

|

|

17.

|

In a supply curve the

horizontal axis measures _____ while in a demand curve the horizontal axis measures _____

.

a. | supply -

supply | c. | supply -

demand | b. | demand - demand | d. | demand - supply |

|

|

|

Supply and

Elasticity

In Chapter 4,

you learned that elasticity of

demand measures how consumers will

react to a change in price.

Elasticity of supply is based on the same concept. Elasticity of supply is a measure of

the way suppliers respond to a change in price.

Elasticity of supply tells how firms will

respond to changes in the price of a good. The labels elastic, inelastic, and unitary

elastic represent the same values of elasticity of supply as those of elasticity of

demand.

|

When elasticity is greater than one, supply is very sensitive to changes

in price and is considered elastic. If supply is not very responsive to changes in price, and

elasticity is less than one, supply is considered inelastic. When a percentage change in price is

perfectly matched by an equal percentage change in quantity supplied, elasticity is exactly one, and

supply is unitary elastic. | | |

|

|

|

18.

|

What does elasticity of supply

measure?

a. | how suppliers respond to a change in

demand | c. | how demand affects

price | b. | how suppliers respond to a change in price | d. | how consumers react to a change in

supply |

|

|

|

19.

|

Elastic, inelastic,

and unitary elastic

represent the same values of elasticity of supply as those of elasticity of

demand.

|

|

|

20.

|

When a percentage change in

price is perfectly matched by an equal percentage change in quantity supplied, elasticity is exactly

one and supply is

a. | unitary

elastic | c. | inelastic | b. | elastic |

|

|

|

21.

|

If supply is not very

responsive to changes in price, and elasticity is less than one, supply is considered

a. | elastic | c. | unitary elastic | b. | inelastic |

|

|

|

22.

|

When elasticity is greater than

one, supply is very sensitive to changes in price and is considered

a. | elastic | c. | unitary elastic | b. | inelastic |

|

|

|

Elasticity of Supply and Time

What determines whether the supply of a good will be

elastic or inelastic? The key factor is time. In the short run, a firm cannot easily change its

output level, so supply is inelastic. In the long run, firms are more flexible, so supply is more

elastic.

Elasticity

of Supply in the Short Run

An orange grove is one example of a

business that has difficulty adjusting to

a

change in price in the short term. Orange

trees take several years to mature and grow fruit.

If the price of oranges goes up, an

orange grower can buy and plant more

trees, but he will

have to wait several years

for his investment to pay off. In the short

term, the grower could

take smaller steps

to increase output. For example, he could

use a more effective pesticide.

While this

step might increase his output somewhat, it

would probably not increase the number

of

oranges by very much. Economists would

say that his supply is inelastic, because

he

cannot easily change his output. The same

factors that prevent the owner of the

orange

grove from expanding his supply

will also prevent new growers from

entering the market and

supplying oranges

in the short term.

In the short run, supply is inelastic

whether the

price increases or decreases. If

the price of a crate of oranges falls, the

grove owner has few

ways to cut his supply.

He invested years ago in land and trees, and

his grove will provide

oranges no matter

what the price is. Even if the price drops

drastically, the grove owner will

probably

pick and sell nearly as many oranges as

before. The grove owner’s competitors

have

also invested heavily in land and trees and

won’t drop out of the market if they

can

survive. In this case, supply is inelastic

whether prices rise or fall.

|

While orange groves illustrate a business

in which supply is inelastic,

other businesses

benefit from more elastic supply.

For example, a business that provides

a

service, such as a haircut, is highly elastic.

Unlike oranges, the supply of haircuts

is

easily expanded or reduced. If the price

rises, barber shops and salons can hire

workers

quickly.

In addition, new barber shops and

salons will open, and existing

businesses

might stay open later in the evening. This

means that a small increase in price will

cause a large increase in quantity supplied,

even in the short term.

If the price of a

haircut drops, some

barbers will close their shops earlier in the

day, and others will leave

the market for

jobs elsewhere. Quantity supplied will fall

quickly. Because haircut suppliers

can

quickly change their operations, the supply

of haircuts is elastic.

| | |

|

|

|

23.

|

What is the key factor that

determines if the supply of a good will be elastic or inelastic?

a. | supply | c. | time | b. | demand | d. | substitutes |

|

|

|

24.

|

Because companies can’t

easily change production quickly, supply is

a. | elastic | c. | varied | b. | inelastic | d. | costly |

|

|

|

25.

|

When companies have more time

to change production, supply becomes more

a. | elastic | c. | plentiful | b. | inelastic | d. | costly |

|

|

|

26.

|

In the short run, automobile

factories tend to be _____ while donut shops tend to be _____ .

a. | inelastic -

elastic | c. | inelastic -

inelastic | b. | elastic -inelastic | d. | elastic - elastic |

|

|

|

Elasticity

in the Long Run

Like

demand, supply can become more

elastic over time. Consider the example of

the orange grower who

could not increase

his output much when the price of oranges

rose. Over time, he could plant

more trees

to increase his supply of oranges. These

changes will become more effective

over

time as trees grow and bear fruit. After

several years, he will be able to sell

many

more oranges at the high market price.

|

If the price drops and stays low

for

several years, orange growers who survived

the first two or three years of losses

might

decide to give up and grow something else.

Given five years to respond instead of

six

weeks, the supply of oranges will be far

more elastic. Just like demand, supply

becomes

more elastic if the supplier has a

long time to respond to a price

change. | | |

|

|

|

27.

|

When companies have enough time

to change their production demand and supply can become

a. | inelastic | c. | more costly | b. | elastic | d. | more scarce |

|

|

|

|

|

|

28.

|

If supply is inelastic, how

will supply react to a small increase in price?

a. | there will be a big change in

supply | c. | supply will change but very

little | b. | supply will not change at all | d. | price has no effect on supply |

|

|

|

29.

|

Which two actions, taken by

firms comprise the law of supply? (pick 2)

|

|

|

a. | quantity

supplied | f. | variable | b. | market supply schedule | g. | market supply curve | c. | supply | h. | supply schedule | d. | elasticity of supply | i. | supply curve | e. | law of supply |

|

|

|

30.

|

a chart that lists how much of a good a supplier will

offer at different prices

|

|

|

31.

|

the amount a supplier is willing and able to supply at

a certain price

|

|

|

32.

|

a graph of the quantity supplied of a good by all

suppliers at different prices

|

|

|

33.

|

the amount of goods available

|

|

|

34.

|

a measure of the way quantity supplied reacts to a

change in price

|

|

|

35.

|

tendency of suppliers to

offer more of a good at a higher price

|

|

|

36.

|

a graph of the quantity supplied of a good at different

prices

|

|

|

37.

|

a factor that can change

|

|

|

38.

|

a chart that lists how much

of a good all suppliers will offer at different prices

|