|

|

|

|

|

|

1.

|

Examine the information above.

On the right, list the things you expect to learn from this lesson.

Review the vocabulary words

and look for them as you work through the lesson. You will be tested on them

later.

|

|

|

The marginal product of labor is the increase in output

added by the last unit of labor. In

Section 1, we identified how producers respond to a change in price. The law of supply states that

producers will offer more goods as the price goes up and fewer as the price falls. In this section,

we will explain how a supplier decides how much to produce.

Consider a firm that

produces beanbags The firm’s factory has one sewing machine and one pair of scissors. The

firm’s inputs are workers and materials, including cloth, thread, and beans. Assume that each

beanbag requires the same amount of materials. As the number of workers increases, what happens to

the quantity of beanbags produced? | Labor and

Output

One of the basic

questions any business owner has to answer is how many workers to hire. To answer this question,

owners have to consider how the number of workers they hire will affect their total production. For

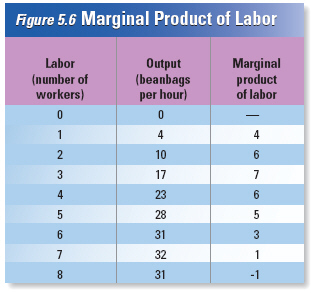

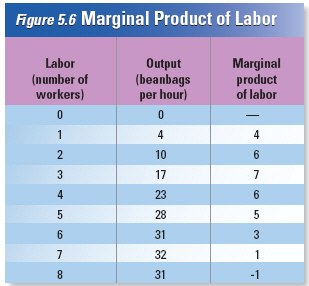

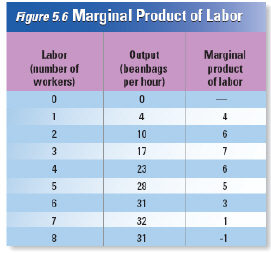

example, at the beanbag factory, one worker can produce four beanbags per hour. Two workers can make

a total of ten bags per hour, and three can make a total of seventeen beanbags an hour. As new

workers join the company, total output increases. After the seventh worker is hired, production peaks

at 32 beanbags per hour. When the firm hires the eighth worker, however, total output drops to 31

bags per hour.

Figure 5.6 shows the relationship between labor, measured by the number of

workers in the factory, and the number of beanbags produced. | | |

|

|

|

2.

|

Why does the marginal product

of labor decrease with more than four workers in this

example?

a. | They did not hire enough

workers | c. | They do not have

enough material to increase production | b. | Production is limited by the equipment needed to increase

production | d. | They need to increase wages to

increase production |

|

|

|

3.

|

At what point does an increase

in hiring actually decrease the number of beanbags produced?

a. | 4

workers | c. | 7

workers | b. | 6 workers | d. | 8 workers |

|

|

|

Marginal

Product of Labor

The

third column of Figure 5.6 shows the

marginal product of labor, or the change in

output

from hiring one more worker. This

is called the marginal product because it

measures the change

in output at the

margin, where the last worker has been

hired or fired. | The first worker

to be hired produces

four bags an hour, so her marginal product

is four bags. The second worker

raises total

output from four bags an hour to ten, so her

marginal product of labor is six.

Looking

at this column, we see that the marginal

product of labor increases for the first

three

workers, rising from four to seven. | | |

|

|

|

4.

|

How many workers produces the

highest marginal product of labor?

|

|

|

5.

|

Which statement is

true?

a. | Hirering more workers always results

in more production | c. | Hiring more

workers never results in more production | b. | Hiring more workers does not necessarily result in more

production | d. | There is no way to tell how many

workers will increase production |

|

|

|

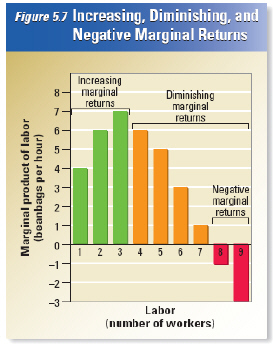

Increasing

Marginal Returns

The

marginal product of labor increases for the first three workers because there are three tasks

involved in making a beanbag. Workers cut and sew cloth into the correct shape, stuff it with beans,

and sew the bag closed. In our example, a single worker performing all these tasks would only produce

four bags per hour. Adding a second worker would allow each worker to specialize in one or two tasks.

If each worker focuses on only one part of the | process, she will waste less time

switching between tasks and will become more skillful at her assigned tasks. In other words,

specialization increases output per worker, so the second worker adds more to output than the first.

The firm enjoys increasing marginal

returns.

In our example, there are benefits from specialization for the first three

workers. The firm enjoys a rising marginal product of labor for the first three

workers. | | |

|

|

|

6.

|

How many tasks are required to

produce a bean bag?

|

|

|

7.

|

What effect does specialization

have on the production of bean bags?

a. | it increases the productivity of the

workers | c. | it decreases the

marginal productivity no matter how many workers are hired | b. | it decreases the productivity of the

workers | d. | it has no effect on

productivity |

|

|

|

Diminishing

Marginal Returns

When

the fourth through the seventh workers are hired, the marginal product of labor is still positive.

Each new worker still adds to total output. However, the marginal product of labor shrinks as each

worker joins the company. The fourth worker increases output by six bags, while the seventh increases

output by only one bag. Why?

After the beanbag firm hires its first three workers, one for

each task, the benefits of specialization end. At that point, adding more workers increases total

output, but at a decreasing rate. This situation is known as diminishing marginal returns. A

firm with diminishing marginal returns of labor will produce less and less output from each

additional unit of labor added to the mix.

The firm suffers from diminishing marginal returns

from labor because its workers must work with a limited amount of capital. Remember that capital is

any human-made resource that is used to produce other goods. In this example, capital is represented

by the factory’s single sewing machine and pair of scissors.

| When there are

three workers, but only one needs to use the sewing machine, this worker will never have to wait to

get to work. When there are more than three workers, the factory will assign more than one to

work at the sewing machine. While one is working, the other will have to wait. She may be able to

help cut fabric or stuff bags in the meantime, but every bag must be sewn up at some point, so she

cannot greatly increase the speed of the production process.

The problem gets worse as more

workers are hired and the amount of capital remains constant. Wasted time waiting for the sewing

machine or scissors means that additional workers will add less and less to total output at the

factory.

Negative Marginal Returns

As the table in Figure 5.6 shows,

adding the eighth worker at the beanbag factory can actually decrease output by one bag. At this

stage, workers get in each other’s way and disrupt the production process, so overall output

decreases. Of course, few companies ever hire so many workers that their marginal product of labor

becomes negative | | |

|

|

|

8.

|

At that point does adding more

workers increases total output, but at a decreasing rate.

a. | 4

workers | c. | 7

workers | b. | 5 workers | d. | 8 workers |

|

|

|

9.

|

What do they call it when you

add more workers that increases total output but at a decreasing rate?

a. | productivity

enhancement | c. | increasing

marginal returns | b. | specialization | d. | diminishing marginal returns |

|

|

|

10.

|

What is the biggest impediment

to specialization and increasing marginal productivity?

a. | land | c. | capital | b. | labor | d. | finance |

|

|

|

Labor has increasing and then diminishing

marginal returns.

|

|

|

11.

|

What is the marginal product of

labor when the factory currently employs five workers?

|

|

|

12.

|

Look at the chart on the right.

Remember that labor is expensive. How many workers would you hire to maximize specialization and

productivity?

|

|

|

Production

Costs

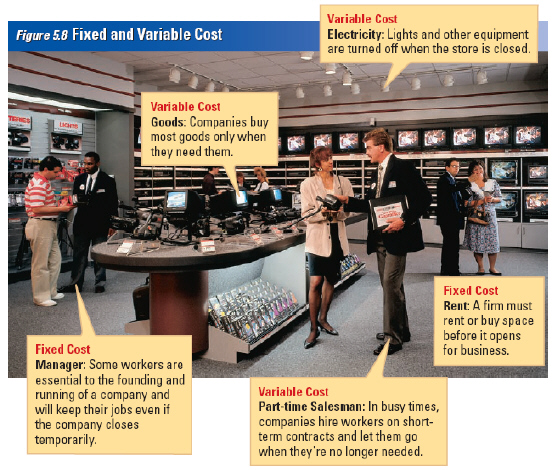

Paying workers and

purchasing capital are all costs of producing goods. Economists divide a producer? ’s costs

into two categories: fixed costs and variable costs.

|

|

|

13.

|

Firms must separate fixed costs

from variable costs to determine whether or not to

produce at a given market price. Why are some

employees considered variable costs?

a. | They are essential to running the

company and must be paid no matter what | c. | They are always full time employees | b. | They are non-essential and the company can do without them

if necessary. Their usefulness varies from time to time | d. | They do work essential for the company to make a

profit |

|

|

|

14.

|

Rent and utilities are

considered

a. | fixed

costs | c. | marginal

expenditures | b. | variable costs | d. | capital |

|

|

|

Firms consider a variety of costs when deciding how

much to produce. Firms consider a variety of costs when deciding how

much to produce. Fixed

Costs

A fixed cost

is a cost that does not change, no matter how much of a good is produced. Most fixed costs

involve the production facility, the cost of building and equipping a factory, office, store, or

restaurant. Examples of fixed costs include rent, machinery repairs, property taxes on a factory, and

the salaries of workers who keep the business running even when production temporarily

stops.

| Variable

Costs

Variable costs

are costs that rise or fall depending on the quantity produced. They include the costs of raw

materials and some labor. For example, to produce more beanbags, the firm must purchase more beans

and hire more workers to stuff the beanbags. If the company wants to produce less and cut costs, it

can stop buying beans or have some workers work fewer hours a week. The cost of labor is a variable

cost because it changes with the number of workers, which changes with the quantity produced.

Electricity and heating bills are also variable costs, because the company can cut off heat and

electricity for the factory and its machines when they are not in use. | | |

|

|

|

15.

|

What is the total cost of

producing 7 bean bags?

|

|

|

16.

|

How many bean bags will give

you the greatest profit?

|

|

|

17.

|

Would you rather take in $216

or $240 in total revenue?

a. | $240 because you make more

profit | c. | Neither is enough to sustain the

business | b. | $216 because costs are not as high | d. | It doesn’t matter because they both yield the same amount of

profit |

|

|

|

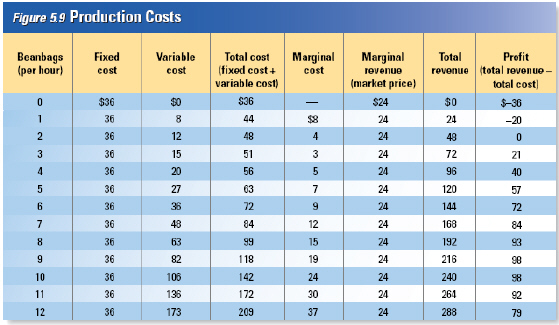

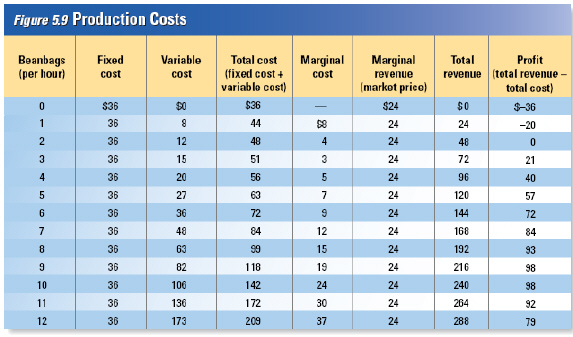

Total

Cost

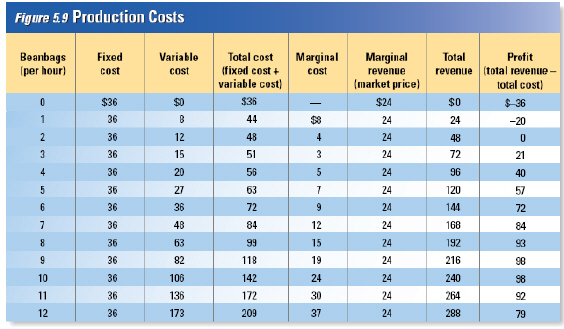

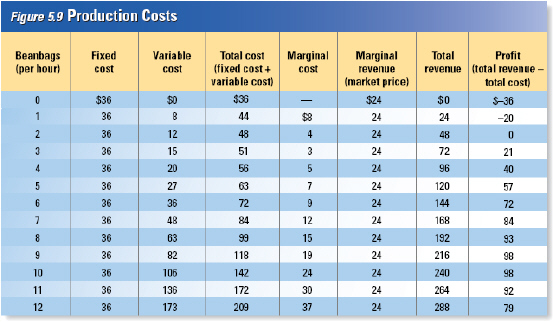

Figure 5.9 shows

some cost data for the firm that produces beanbags. The firm has a factory that is fully equipped to

produce beanbags. How does the cost of producing beanbags change as the output increases?

In

our example, the fixed costs are the costs of the factory building and all the machinery and

equipment inside. As shown in the second column in Figure 5.9, the fixed costs are $36.00 per

hour.

Variable costs include the cost of beans, fabric, and most of the workers hired to

produce the beanbags. As shown in the third column, variable costs rise with the number of beanbags

produced. Fixed costs and variable costs are added together to find total cost. Total cost is

shown in the fourth column.

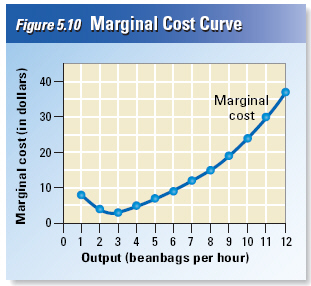

| Marginal

Cost

If we know the

total cost at several levels of output, we can determine the marginal cost of production at

each level. Marginal cost is the additional cost of producing one more unit.

As shown in

Figure 5.9, even if the firm is not producing a single beanbag, it still must pay $36.00 an hour for

fixed costs. If the firm decides to produce just one beanbag an hour, its total cost rises $8.00 from

$36.00 to $44.00 an hour. The marginal cost of the first beanbag is $8.00.

For the first three

beanbags, the marginal cost falls as output increases. The marginal cost of the second beanbag is

$4.00, and the marginal cost of the third beanbag is $3.00. Each additional beanbag is cheaper to

make because of increasing marginal returns resulting from specialization.

With the fourth

beanbag, the marginal cost starts to rise. The marginal cost of the fifth per hour is $7.00, the

sixth costs $9.00, and the seventh, $12.00. The rising marginal cost reflects diminishing returns to

labor. The benefits of specialization are exhausted at three beanbags per hour, and diminishing

returns set in as more and more workers share a fixed production facility. | | |

|

|

|

18.

|

At what point does the marginal

cost of producing beanbags begin to rise?

a. | 3 bags | c. | 6 bags | b. | 4 bags | d. | 8 bags |

|

|

|

19.

|

So what does the marginal cost

of production tell the businessman?

a. | The cost in production by adding

additional workers | c. | Whether or not to

increase supply | b. | The total revenue taken in | d. | The projected demand for his

products |

|

|

|

Setting Output Setting Output

Behind all of the decisions about how many workers

to hire is the firm’s basic goal: to maximize profits. Profit is defined as total revenue minus

total cost. As you read in Chapter 4, a firm’s total revenue is the money the firm gets by

selling its product. Total revenue is equal to the price of each good multiplied by the number of

goods sold. Figure 5.9 shows total revenue when the price of a beanbag is $24.00. To find the level

of output with the highest profit, we look for the biggest gap between total revenue and total cost.

The gap is biggest and profit is highest when the firm makes 9 or 10 beanbags per hour. At this rate,

the firm can expect to make a profit of $98.00 an hour.

|

|

|

20.

|

Why wouldn’t you make, at

least, some profit by producing 2 beanbags?

a. | Because there is not enough total

revenue | c. | because total

costs equal total revenue | b. | Because fixed costs are higher than variable

costs | d. | because total revenue is only

$10 |

|

|

|

21.

|

If you don’t produce any

beanbags, why are you loosing money?

a. | Because fixed costs still have to be

paid | c. | Because there are not enough

workers | b. | Because variable costs are not high enough | d. | Because you still have to pay the fixed

costs |

|

|

|

Marginal

Revenue and Marginal Cost

Another way to find the best level of output is to find the output level where

marginal revenue is equal to marginal cost. Marginal revenue is the additional income from

selling one more unit of a good. If the firm has no control over the market price, marginal revenue

equals the market price. Each beanbag sold at $24.00 increases the firm’s total revenue by

$24.00, so marginal revenue is $24.00.

According to the table, price equals marginal cost

with 10 beanbags, so that’s the quantity that maximizes profit at $98 an hour.

To

understand how an output of 10 beanbags maximizes the firm’s profits, suppose that the firm

picked a different level of output. If the firm made only 4 beanbags per hour, is it making as much

money as it can? From Figure 5.9, we know that the marginal cost of the fifth beanbag is $7.00.

The market price for a beanbag is $24.00, so the marginal revenue from that beanbag is $24.00. The

$17.00 difference between the marginal revenue and marginal cost represents pure profit for the

company from making and selling the fifth beanbag. The company should increase its production to five

beanbags an hour to capture that profit on the fifth beanbag.

| If we do the same calculations for a sixth

beanbag, we find that the company can capture a profit of $15.00 by producing the sixth beanbag per

hour. The price of the seventh beanbag is $12.00 higher than its marginal cost, so that beanbag earns

an additional $12.00 in profit for the company. The profit is available any time the company receives

more for the last beanbag than it cost to produce. Any rational entrepreneur would take this

opportunity to increase profit.

Now suppose that the firm is producing so many beanbags an

hour that marginal cost is higher

than price. If the firm produces eleven beanbags an hour, it receives $24.00 for that eleventh

beanbag, but the $30.00 cost of that beanbag wipes out the profit. The firm actually loses $6.00 on

the sale of the eleventh beanbag. Because marginal cost is increasing, and price is constant in this

example, the losses would get worse at higher levels of output. The company would be better off

producing less and keeping costs down.

The ideal level of output is where marginal revenue

(price) is equal to marginal cost. Any other quantity of output would generate less

profit.

| | |

|

|

|

22.

|

Why would we try to find the

output level of marginal revenue that is equal to marginal cost?

a. | to find the best level of

input | c. | to determine the price of

products | b. | to find the best level of output | d. | to determine the cost of capital |

|

|

|

23.

|

What is marginal

revenue?

a. | the difference between capital and

labor | c. | the additional cost of selling all

goods | b. | the additional cost from selling one more unit of a

good | d. | the additional income from selling one more unit of a

good |

|

|

|

24.

|

According to the table, price

equals marginal cost with _____ beanbags, so that’s the quantity that maximizes profit at $98

an hour.

|

|

|

25.

|

Look at the chart above. Is it

possible for this company to produce so many beanbags that they loose money by producing them?

a. | yes | c. | the chart does not show

this | b. | no | d. | Silly, it is obvious that the more

beanbags you produce the more money you will make |

|

|

|

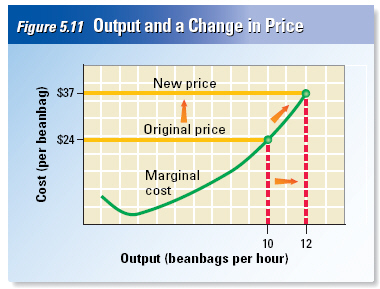

Responding

to Price Changes

What

would happen if the price of a beanbag rose from $24.00 to $37.00? Thinking at the margin, we would

predict that the firm would increase production to twelve beanbags per hour. That’s the

quantity at which the marginal cost is equal to the new, higher price. At the original price of

$24.00, the firm would not produce more than ten beanbags, according to

Figure 5.11. When the

price rises to $37.00, marginal revenue soars above marginal cost at that output level. Raising

production to twelve beanbags an hour would allow the firm to capture profits on the eleventh and

twelfth beanbags. |

This example shows the law of supply in

action. An increase in price

from $24.00

to $37.00 causes the firm to increase the

quantity supplied from ten to

twelve

beanbags an hour.

| | |

|

|

|

26.

|

If the price of beanbags

remains at $24 the company will loose money by increasing supply (production) What happens if they

increase the price from $24 to $37

a. | the company will still loose

money | c. | the companies profits will remain

the same | b. | the companies profits will go up | d. | increasing price has no effect on

supply |

|

|

|

27.

|

This chart is an illustration

of the law of _____ .

a. | supply | c. | equilibrium | b. | demand | d. | falling revenues |

|

|

|

The Shutdown Decision The Shutdown Decision

Consider the problems faced by a factory

that is losing money. The factory is producing at a level of output at which marginal revenue

is equal to marginal cost. As you have read, this is the most profitable level of output. However,

the market price is so low that the factory’s total revenue is still less than its total cost,

and the firm is losing money. Should this factory continue to produce goods and lose money, or should

its owners shut the factory down? This may seem like a silly question. In fact, there are times when

keeping a money-losing factory open is the best choice. The firm should keep the factory open if the

total revenue from the goods and services the factory produces is greater than the cost of keeping it

open.

For example, if the price of beanbags drops to $7, and the factory produces at the

profit-maximizing level of five beanbags per hour, the total revenue of the business is $35 per hour.

Weigh this against the factory? ’s operating cost, or the cost of operating the

facility. The operating cost includes the variable costs the owners must pay to keep the factory

running, but not the fixed costs, which the owners must pay whether the factory is open or

closed.

According to Figure 5.9, if the factory produces five beanbags, the variable cost is

$27 per hour. Therefore, the benefit of operating the facility (total revenue of $35) is greater than

the variable cost ($27), so it makes sense to keep the facility running.

Consider the effects

of the other choice. If the firm were to shut down the factory, it would still have to pay all of its

fixed costs. The factory? ’s total revenue would be zero because it would be producing nothing

for sale. Therefore, the firm would lose an amount of money equal to its fixed costs.

For this

beanbag factory, the fixed costs equal $36 per hour, so the factory would lose $36 for each hour it

is closed. If the factory were to keep producing five beanbags per hour, its total cost would be $63

($36 in fixed costs plus $27 in variable costs) per hour, but it would lose only $28 ($63 in total

cost minus $35 in revenue) for each hour it is open. The factory would lose less money while

producing because the total revenue ($35) would exceed the variable costs ($27), leaving $8 to cover

some of the fixed costs. Although the factory would lose money in either situation, it would lose

less money by continuing to produce and sell beanbags.

How long will a business continue to

operate a factory at a loss before it decides to replace the facility? The firm will build a new

factory and stay in the market only if the market price of beanbags is high enough to cover all the

costs of production, including the cost of building a new factory.

|

|

|

28.

|

When should a company keep its

factory open even though it is loosing money?

a. | You will make more profits once you

hire more workers and increase production of beanbags | c. | To benefit the workers who would loose their jobs if the factory

closed | b. | The firm should keep the factory open if the total revenue from the goods and

services the factory produces is lower than the cost of keeping it open.

| d. | The firm should keep the factory open if the total revenue

from the goods and services the factory produces is greater than the cost of keeping it open.

|

|

|

|

29.

|

Even though you may shut down

an unprofitable factory, you would still have to pay the

a. | variable

costs | c. | supply

costs | b. | labor costs | d. | fixed costs |

|

|

|

For

most firms, the marginal cost of production falls as output rises from zero, but eventually begins to

rise.

|

|

|

30.

|

How many beanbags an hour

should this firm make to produce at the lowest possible marginal cost?

|

|

|

a. | fixed cost

| f. | increasing marginal

returns | b. | marginal cost | g. | operating cost | c. | marginal product of labor | h. | diminishing marginal returns | d. | marginal revenue | i. | variable cost | e. | total cost |

|

|

|

31.

|

a level of production in

which the marginal product of labor decreases as the number of workers

increases

|

|

|

32.

|

a cost that does not change,

no matter how much of a good is produced

|

|

|

33.

|

the change in output from

hiring one additional unit of labor

|

|

|

34.

|

fixed costs plus variable

costs

|

|

|

35.

|

a cost that rises or falls

depending on how much is produced

|

|

|

36.

|

the additional income from

selling one more unit of a good; sometimes equal to price

|

|

|

37.

|

a level of production in

which the marginal product of labor increases as the number of workers

increases

|

|

|

38.

|

the cost of operating a

facility, such as a store or factory

|

|

|

39.

|

the cost of producing one

more unit of a good

|